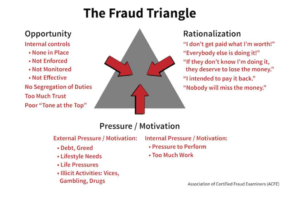

The ‘fraud triangle’ (shown below) is a well-known tool for enabling discussions among audit teams about the possible ‘climatic’ factors that may be present in an audit client. Where all three coincide, fraud is much more likely to be present.

ISA 240 ‘The Auditor’s Responsibilities Relating to Fraud in an Audit of Financial Statements’ was re-issued in October 2022 with additional requirements (among other topics) to do with the audit engagement team discussion.

For the purposes of this blog (Part 1 of a 2 part series) we are focusing on the main areas of the audit team discussion.

‘The discussion shall include an exchange of ideas among engagement team members about fraud risk factors, including:

- incentives for management or others within the entity to commit fraud;

- how management could perpetrate and conceal fraudulent financial reporting; and

- how assets of the entity could be misappropriated (ISA 240.16.1)

For a group audit, the discussion among the group engagement team shall include matters to discuss with the component auditor of a significant component about the susceptibility of the component to material misstatement of the financial information of that component due to fraud. (ISA 240.16.2)

If allegations of fraud come to the auditor’s attention, the discussion shall include how to investigate and respond to those allegations. (ISA 240.16.3) see last week’s blog on the expanded Protected Disclosures regime now in force in Ireland and which will have implications for auditors of the affected entities.

The standard allows for the initial engagement team discussion to be later revisited and revised, where necessary, when ‘fraud risk factors that have been identified during the course of the audit and the implications for the audit’ considered (ISA 240.16.4)

Basically the audit engagement team is expected to document a discussion of how fraud might be perpetrated in the audit client. That discussion needs to be structured around the headline items shown below:

The guidance focuses on:

- incentives to manage earnings or key performance indicators derived from the financial statements in order to deceive financial statement users by influencing their perceptions as to the entity’s performance and profitability;

- A consideration of circumstances that might be indicative of earnings management and the practices that might be followed by management to manage earnings that could lead to fraudulent financial reporting.

- A consideration of the risk that management may attempt to present disclosures in a manner that may obscure a proper understanding of the matters disclosed (for example, by including too much immaterial information or by using unclear or ambiguous language).

- A consideration of the known external/internal factors affecting the entity that may create an incentive or pressure for management or others to commit fraud, provide the opportunity for fraud to be perpetrated, and indicate a culture or environment that enables management or others to rationalize committing

Further guidance on these topics is given in Application paragraphs A12 and A12-1 in the standard. We will say more about this topic next week.

IT Controls Assessment

Auditors are reminded that there are relatively significant changes in the requirements of ISA 315 Identifying And Assessing The Risks Of Material Misstatement for accounting periods commencing 15 December 2021, which in practical terms means, accounting periods Ended 31 December 2022 and later.

Auditors dealing with the audits of entities with such accounting periods affected by these change will need, to adopt new audit programmes and, in additional to the normal audit tests, to also assess the entity’s IT controls (no ,matter what the size of that entity).

This is a significant new development for auditors of SMEs, in particular, and will be a game changer ion the type of audit documentation and evidence of assessment of such IT controls by the auditor on audit files.

For an easy to implement additional (two page) IT Controls Questionnaire to help document the above process, please click on this link to download immediately for only €60 + VAT.

Please go to our website to see our:

- Anti-Money Laundering Policies Controls & Procedures Manual (March 2022) – View the Table of Contents click here.

- AML webinar (March 2022) available here, which accompanies the AML Manual. It explains the current legal AML reporting position for accountancy firms and includes a quiz. Upon completion, you receive a CPD Certificate of attendance in your inbox.

- letters of engagement and similar templates. Please visit our site here where immediate downloads are available in Word format. A bulk discount is available for orders of five or more items if bought together.

- ISQM TOOLKIT or if you prefer to chat through the different audit risks and potential appropriate responses presented by this new standard, please contact John McCarthy FCA by e-mail at john@jmcc.ie.

We typically tailor ISQM training and brainstorming sessions to suit your firm’s unique requirements. The ISQM TOOLKIT 2022 is available to purchase here.