by John McCarthy Consulting Ltd. | Feb 25, 2020 | Blog, News

Many accountants and auditors are working hard this week to assist primary and post-primary schools around Ireland meet the 28 February 2020 deadline set by the Financial Support Services Unit (FSSU) for the filing of schools’ annual financial statements.

The Education Act, 1998 (the Act) is the relevant legislation that governs this area but it’s out of line with the latest thinking on accounting and legal language used in the Companies Act, 2014 in Ireland.

When compared to this later legislation, The Education Act is found to be inadequate in at least these three areas:

- The Act speaks about ‘all proper and usual accounts’ instead of ‘adequate accounting records’ used in the Companies Act, 2014;

- The Act, is vague about whether the financial statements should give a ‘true and fair view’, which, clearly, they should;

- The Act does not specify precisely the financial reporting framework that ought to be best applied to school accounting, which is now FRS 102, (The Financial Reporting Standard Applicable in the UK and the Republic of Ireland).

This single financial reporting standard applies to the financial statements of entities that are not applying EU-adopted IFRS, FRS 101 or FRS 105. It came into being in 2015, and Section 1A of that Standard came into being in January 2017, well after the Education Act was written. FRS 102 replaced the earlier version of Irish Generally Accepted Accounting Practice (GAAP), to which the Act refers, which had been in place for about 45 years.

New International Audit Standards (ISAs) were enacted for Ireland in June 2016 and the Act does not refer to these either.

Interim solution for Accountants / Auditors

Clearly the Education Act, 1998 needs a refresh from an accounting and audit perspective. In the meantime, these deficiencies are causing a technical difficulty for reporting accountants and auditors in helping schools meet the February deadline.

In an effort to help reporting accountants with this work, we have created a set of four templates, which address the inadequacies of the Act and clarify state how best to achieve a true and fair view in the midst of these inadequacies, through greater disclosure etc.

The templates are:

- Audit assignment engagement letter template under FRS 102

- Audit assignment representation letter template under FRS 102

- Audit exempt compilation assignment engagement letter template under FRS 102

- Audit exempt compilation assignment representation letter template under FRS 102

They templates are available for purchase on our website here for €50 each and may be downloaded immediately as Word templates for easy adaptation.

Have you prepared an AML Business-Wide Risk Assessment which is required if you have an AML Inspection visit? There is a template available and a webinar on how to prepare it. Both of these help firms comply with the latest requirements of Section 30A of the Criminal Justice (Money Laundering and Terrorist Financing) Acts, 2010 to 2018.

For many other webinar topics including Investment Property Accounting, FRS 105, Common Errors in FRS 102 Accounting and the latest on FRS 105 and company law, visit our online webinar training website.

by John McCarthy Consulting Ltd. | Jun 18, 2014 | News

Welcome to another of our regular blogs on topical issues for accountants in practice.

Our last blog https://jmcc.ie/d7/node dealt with engagement letters in general and focused on audit and audit exempt engagement letters. This blog targets tax engagement letters specifically.

Engagement letter fundamentals – an important line of defence

Tightening the language used in tax and other engagement letters will help limit your professional liability.

In recent times we have noticed a renewed interest by accountancy firms in having well written and up to date engagement letters reviewed and critiqued by risk management professionals. The objective of this article is to outline the fundamentals of tax and other types of engagement letters and to suggest provisions that will help minimize legal liability faced by accountants in practice.

Professional liability insurers and solicitors specialising in professional negligence claims will often agree that engagement letters are one of the first lines of defence in a professional negligence claim against an accountant. When drafted properly, engagement letters form the basis for an enforceable contract and should have caveats unique to the scope of the service provided, the amount of risk inherent in the engagement, and the need to satisfy professional standards.

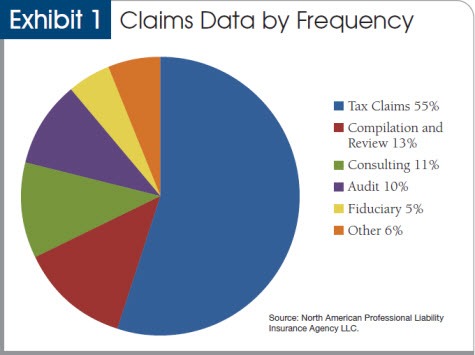

The majority of claims (by frequency) reported by leading professional indemnity insurers arise from tax services, yet, according to our experience, individual tax engagements are where engagement letters are least used. Recent data (January 2014) we have seen from claims arising in the USA show that well over half the claims (by number) arise from tax services.

While the advice that follows is focused on tax engagement letters, the same principles apply to most other types of engagement letter.

Here are some of the fundamental objectives in drafting good engagement letters:

1. Address the letter to the appropriate parties in a formal introductory paragraph. Exclude any taxes not within the scope of the tax return and exclude children of the client or other entities owned by the individual tax client and include the appropriate year or years that are being prepared.

2. Identify which returns are being prepared, and do not combine multiple returns. (For example, do not include a gift tax return service with an income tax return unless the proper disclaimer language for a gift tax return is included.) The following language is highly recommended.

‘We will prepare your [Year] income tax return. This engagement pertains only to the [Year] tax year, and our responsibilities do not include preparation of any other tax returns that may be due to any tax authority, If we receive specific instructions from you about other taxes or other tax years, these assignments will be the subject of separate engagement letters.’

Deal with the price of the service, payment terms, retainers, additional charges for information received late, additional fees. Clarity and diligence must be adhered to, as many professional liability lawsuits, professional body ethical complaints, and loss of clients have resulted from misunderstanding these provisions. Too often, a phrase like the following is used in a standard letter:

‘Our fee for services will be at our standard hourly rate for the personnel assigned to this engagement [or fixed fees to cover other than hourly fee arrangements]. Payment is expected when our services are complete.’’

Consider the following enhancements to the typical clause above:

o Specify more clearly the payment terms.

o If you wish, stipulate that a retainer will be required and will be applied toward the final fee and that the retainer is not an estimate of the fee charged for services.

o Identify when payment is expected.

o Provide for a termination of services if the fee is not paid in full.

o Use an additional charge clause for services not originally contemplated.

o Include a provision for reimbursement for out-of-pocket expenses such as travel, recorded delivery, etc.

3. Use a tax checklist that is sent to clients. The value of a tax checklist in defending a professional liability claim cannot be overstated. However, many tax advisers complain that their clients do not complete the checklist and often return it unopened. Accountants and tax advisers need to get the client to take responsibility for completing the checklist. The language used in the engagement letter should establish this responsibility:

‘We will prepare the returns from information which you will furnish to us. It is your responsibility to provide all the information required for the preparation of complete and accurate returns. We will furnish you with questionnaires and/or worksheets as needed to guide you in gathering the necessary information. Your use of such forms will assist us in keeping our fee to a minimum. To the extent we render any accounting and/or bookkeeping assistance, it will be limited to those tasks we deem necessary for preparation of the returns’.

Each firm has its own comfort level with respect to risk, and every client relationship varies. For this reason, many more areas should be explored for engagement letters than this article can address and this list is not necessarily exhaustive

Engagement Letter Checklist

The following checklist suggests additional considerations for engagement letters, return preparation, and administrative practices:

Exclusion clause. Because tax services can be broad, an exclusion clause that identifies what services will not be provided can be invaluable. For example, a payroll taxes preparation engagement might exclude subcontractor tax, personal or corporate tax compliance, and Forms P11D preparation.

Deadline for submitting return information. Establishing a date by which the client must provide the information needed to prepare the return is essential.

Limitation on use of the returns. Clients may submit tax returns and/or supporting data (like rental income computations) to third parties in lieu of a financial statement, for which potential liability can be addressed through a clause limiting the circulation of tax returns, supporting data and distribution and/or requiring advance written permission before allowing the client circulate the information to named third parties.

Tax position clauses. Many times, what the client thinks is acceptable will conflict with professional standards. Establish language stating that tax positions taken must satisfy professional standards.

Supporting documentation. Because a Revenue audit or investigation is always a possibility, remind clients of their responsibility to maintain adequate records to support the deductions claimed on the return. Include in the letter a reminder of the length of time for which the records should be maintained.

Revenue Audit or HMRC Investigation. Representing a client in a Revenue Audit may be more involved than the tax return preparation itself, for which many accountants may want to deal in a different manner to the main tax assignment e.g. by allowing for the use of specialist advice. The engagement letter should state that in the event of a Revenue Audit/HMRC Investigation the assignment will be covered by the terms of a separately signed engagement letter.

Outcome or results. The engagement letter is not a marketing device. Never guarantee the outcome or results.

Limitation of liability. Ensure such clauses are used appropriately.

Complaints/best service. Make it clear what the lines of communication are in the event of a dispute or claim (give the contact name for the Partner/Director in your organisation that will primarily handle client complaints) and in the event of failure to reach a satisfactory outcome, give the contact details of your professional body.

If interested in having a template engagement letter that follows the above advice, please see our list of engagement letters available for sale below.

Letters of engagement currently available as follows:

1. Limited company audit ROI

2. Limited company – audit exempt ROI

3. Sole trader NI/UK

4. Sole trader ROI

5. Limited by guarantee company ROI

6. MUD Act company – ROI

7. Northern Ireland/UK audit company

8. Northern Ireland/UK – audit exempt company

9. Taxation planning generally

10. Revenue audit Engagement Letter

11. Corporation Tax Engagement Letter

12. Income Tax Engagement Letter

13. Tax disengagement letter (used when a client has ceased using the firm’s tax services, but without a formal notification being received from the client). This letter sets the record straight, to avoid doubt.

These retail at €50 each +VAT, but we are prepared to do discounts for bulk purchases. Once ordered, you will receive a VAT invoice as well as the appropriate engagement letters by e-mail.

Please send us an e-mail to john@jmcc.ie with the words ‘engagement letter’ in the subject line.