The Office of the Director of Corporate Enforcement (ODCE) recently published their Annual Report for 2020.

The section on the reporting by auditors of indictable offences, makes interesting reading, especially the fact that the greatest increase in reports for any category, has been to do with the falsification of books or documents. This particular category of offence is up from one incidence in 2019 to three in 2020. Perhaps connected with Covid?

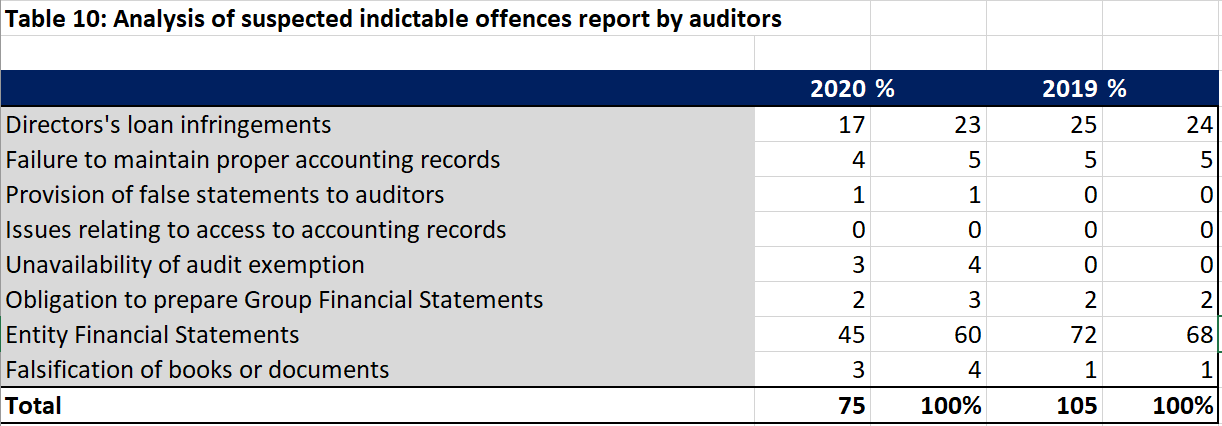

The below table has the details. It should be noted that the number of reports received by the ODCE does not accord with the number of suspected offences reported as, in several instances, the report received includes reference to more than one suspected offence

These types of offence rarely occur in isolation and are often connected with money laundering, because the lack of/falsification of accounting records can often be used to conceal the money laundering activity. Where money laundering is suspected there is a requirement for simultaneous reporting to An Garda Síochana and Revenue, a topic we discussed in an earlier blog.

You can download and read the full ODCE report here.

For more about accountants’ AML compliance obligations, see our AML Policies, Controls & Procedures Manual for 2021.

The Manual contains all the latest requirements relevant to accountants contained in the Criminal Justice (Money Laundering and Terrorist Financing) Acts 2010 to 2021 now fully in force.

For more blogs please visit this link and for our publications and manuals and services click on the hyperlinked words.