by John McCarthy Consulting Ltd. | Sep 6, 2023 | News

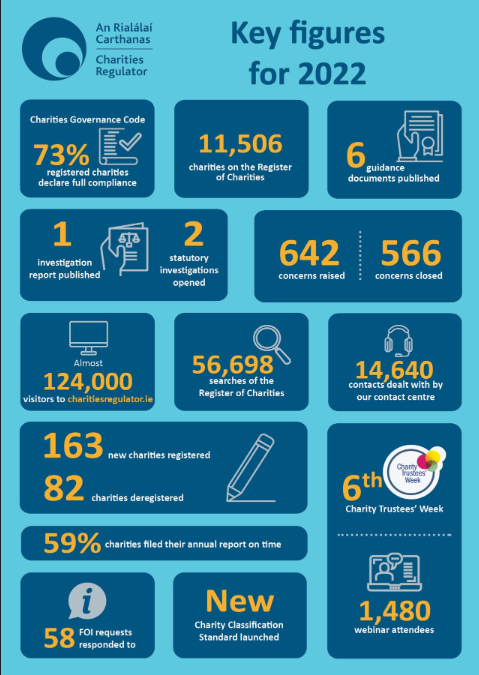

The Charities Regulatory Authority (CRA) published its 2022 Annual Report in July 2023.

The Annual Report shows some interesting developments across the charity sector. Some headlines are:

- Almost three-quarters (73%) of registered charities declared full compliance with the Charities Governance Code.

- On the downside, only two out of every five charities filed an annual report to the CRA on time during 2022. All charities are legally required to file such a report within 10 months of their financial year-end. The contents of these reports are published on the Register of Charities and provide essential information to help inform donors and the general public.

- 41% of registered charities are legally formed as companies, followed by schools representing 32% of registered charities.

- Nearly one in five registered charities had annual income in 2022 of less than €10,000.

Auditors of charities that have accounting years ended 31 December 2022 and later will need, in additional to the normal audit tests, to also assess the charity’s IT controls.

For an easy to implement additional (two page) IT Controls Questionnaire to help document the above process, please click on this link to download immediately for only €60 + VAT.

Please go to our website to see our:

- letters of engagement and similar templates. Please visit our site here where immediate downloads are available in Word format. A bulk discount is available for orders of five or more items if bought together.

- ISQM TOOLKIT or if you prefer to chat through the different audit risks and potential appropriate responses presented by this new standard, please contact John McCarthy FCA by e-mail at john@jmcc.ie.

We typically tailor ISQM training and brainstorming sessions to suit your firm’s unique requirements. The ISQM TOOLKIT 2022 is available to purchase here.

by John McCarthy Consulting Ltd. | Apr 7, 2019 | News

Charity audits are high risk, as has been shown in the recent news story about the disciplinary action against the auditors to the former charity Console.

Auditors have always been expected to have relevant knowledge corresponding to the task in hand and it’s important to have a clear understanding of the key risks involved in auditing a charity, especially because various donor agencies such as the HSE, Tusla and Pobal, to name just a few, have high expectations of what auditors can deliver.

One of the criticisms in the 2017 CRA report on Ataxia Ireland was that it ‘did not set formal objectives for the CEO and/or perform a documented appraisal of the CEO’s performance.

One of the webinars on our site helps auditors to gather their thoughts and plan an effective audit, pinpointing the likely areas of risk including:

- Cut-off

- Fraud

- Failure to report related party transactions

- Incomplete income due to failure to invoice for services rendered or records invoice issued

- Non-receipt of income due from funder

- Misapplication of restricted funds

For the answer to this and other questions on the Audit of Charities, go to our website and download the webinar on this topic for just €45. On successful completion, receive a CPD certificate for your newly acquired knowledge. Well done!

There is an accompanying webinar on the Accounting for Charities – also for €45, or you may purchase the two at the same time for €80.

All our webinars are accessible at any time (for 12 months from date of purchase) here.

For the following ready to use charity engagement letters (in Word) available to purchase online (bulk discounts for purchases of 5 or more at the same time) please click on the relevant links:

by John McCarthy Consulting Ltd. | Feb 1, 2016 | News

More on Parts of FRS 102 That Are Not Yet Applicable in the RoI

Following on last week’s blog piece about Section 1A Small Entities FRS 102, which as you know, does not yet apply in the Republic of Ireland (RoI). There was an error in the blog which stated that charities that were formed as companies limited by guarantee were precluded from using the FRSSE (Financial Reporting Standard for Smaller Entities). However, with the enactment of the Companies Act 2014, companies limited by guarantee may qualify as ‘small’ and may therefore use the FRSSE. Apologies for any confusion.

Meanwhile we would like to draw your attention to another matter in FRS 102. There are now twenty exemptions (where there were previously 18) in Section 35, which many companies will be trawling through, as they transition to FRS 102 for the first time.

Two additional exemptions in Section 35, namely 35.10 (u) ‘Small entities – fair value measurement of financial instruments’ and 35.10 (v) ‘Small entities – financing transactions involving related parties’ . These exemptions were included in the September 2015 version of FRS 102, specifically for ‘small’ entities.

The exemptions give some relief from the amortised cost rule on, for example, directors’ loans, but companies in the Republic of Ireland cannot avail of them just yet, because the relevant company legislation underpinning these rules has not been enacted. Hopefully this will follow soon after the forthcoming election.

The mechanics of these exemptions is that they relate to comparative information only. Companies will have to account for the transactions in accordance with FRS 102 for the first reporting period that they are allowed adopt FRS 102 and make an adjustment to opening reserves at the beginning of the first reporting period (as opposed to the date of transition).

For more on FRS 102 see the following:

1. Updated Transition Checklist (February 2016 version), for more information please click here.

To assist you with the transition work – retails for €100+VAT and accompanied by free:

2. FRS 102 Training Course

To learn the latest developments in accounting and the related company law, come along to our FRS 102 Accounting Update on Tuesday 1 March 2016 at the Camden Court Hotel, Dublin 2. Places are limited and are filling steadily.

For booking details please click here.

3. FRS 102 Transition Service

Please ask us about our bespoke FRS 102 Transition Service where we will examine client accounts before/after transition and give you a tailored report explaining the issues arising and whether the transition has been successful or not. To enquire just send an e-mail to john@jmcc.ie

Our next blog on Investment Properties and FRS 102 will follow next week.

by John McCarthy Consulting Ltd. | Jan 15, 2016 | News

FRSSE and Companies Limited by Guarantee

A query came in from a client recently about the application of the FRSSE to charities for 2015. It’s worth repeating here, as general knowledge about the application of the FRSSE. Here is the query ‘I read somewhere that charities in Ireland cannot apply FRSSE and must go to FRS 102 for periods beginning on or after 1st January 2015, because they are classed as public companies, is this correct?’

Our response:

The Financial Reporting Standard for Small Entities 2015 was published in July 2013. It applies for one year only to financial statements of ‘small’ entities (as defined in company law) for accounting periods commencing on/after 1 January 2015.

In order to understand how to apply any standard, it is always a good idea to read the Scope section. The Scope Section is in Part 1.1 and footnote number 9 explains that companies entitled to the small company criteria can use the FRSSE.

I don’t know the date article of the you are referring to, but since 1 June 2015 (under the CA 2014), companies limited by guarantee (including many charities) may now avail of the ‘small’/’medium’ thresholds and file abridged accounts, among other things. See more below. The way in which the CA 2014 was brought into law was unprecedented, as it was based on the date the accounts are approved by the Directors.

Let’s take two companies ‘A’ and ‘B’, both limited by guarantee, with a 31 December 2014 period end. Company ‘A’’s financial statements are approved on 21 May 2015 (i.e. under the Companies Acts 1963 to 2013), while Company ‘B’’s financial statements are approved on 21 June 2015 (under the Companies Act, 2014).

The effect of these approval dates are that Company ‘A’ cannot avail of:

• Audit exemption

• Exemption from the presentation of the Cash flow statement under FRS 1

• Abridged financial statements

• The FRSSE as it is not deemed to be a ‘small’ entity, but the equivalent of a ‘public’ company as the financial statements were approved before the enactment of the Companies Act, 2014.

Company ‘B’ however can avail of:

• Audit exemption, unless it is a charity with income in excess of €100,000 when the Charities Act, 2009 requires it to have an audit

• Exemption from the presentation of the Cash flow statement as it is a ‘small’ entity

• Abridged financial statements

• The FRSSE as it is now deemed to be a ‘small’ entity, unless it is a financially regulated entity i.e. an insurance broker (as well as certain other companies included in Sections 8 and 9 of the FRSSE 2015) as the financial statements were approved on/after the date of enactment of the Companies Act, 2014.