by John McCarthy Consulting Ltd. | Sep 29, 2020 | Blog, News

The Charities Governance Code Explained

In the last few weeks we have covered several topics in relation to Charities in Ireland arising from the 2019 Charities Regulator Report published in the summer.

We have covered the Types of Charities and Charities by the Numbers.

This week we will look at the Charities Governance Code (the Code). The Code explains the minimum standards required to effectively manage and control all registered charities in Ireland. These standards must be applied from 2020. The first year that registered charities will be expected to report on their compliance with the Code will be 2021.

The Governance Code is structured with two main types of charity in mind:

- volunteer-only charities and

- charities with a small number of paid staff

as these types of charity reflect the majority of registered charities in Ireland.

The Code is tailored to encourage charities of all sizes to have better administration, financial and management systems in place. Underpinning the Six Principles are two main types of standard (depending upon the size and complexity of charities) which are

- the ‘core standards’ (of which there are 32 in total) that all charities must apply (including the charity’s main purpose, whether any private benefit arises, goal setting to raise funds, annual review), and

- ‘additional standards’ that only certain charities need apply (including developing strategic and operational plans).

The six principles of governance that all charities must apply are:

- Advancing charitable purpose – how the charity fits into one or more of the four categories of ‘charitable purpose’ as defined in the Charities Act, 2009;

- Behaving with integrity – setting an ethical culture and tone;

- Leading People – providing leadership to volunteers, employees and contractors;

- Exercising control – putting mechanisms in place to abide by all legal and regulatory requirements

- Working effectively – induction training for Board members and running efficient Board meetings, having people with the right mix of skills and experience; and

- Being accountable and transparent – accounting for the money (including producing unabridged financial statements) and being open/transparent about all charity matters.

Who is the Code for?

The Governance Code document should be used by all trustees of any kind of charity, being:

- Committee members;

- Council members; and

- Board members or directors of the charity.

How should the Code be used?

Trustees should make themselves familiar with the six principles of the Code and should consider them when assessing compliance with actions taken within the charity and ensure that documentary evidence is kept demonstrating how the standards are met.

Reporting Compliance

From 2021 every charity must submit an annual return to the Charities Regulator demonstrating compliance with the Code and providing valid reasons for non-compliance.

Charities will use a 20 page Compliance Record Form identifying actions taken to meet the Governance Code standards, while the amount of evidence expected to support the level of compliance will vary, depending on the size and complexity of the charity.

The guide to the Governance Code with which all trustees should be familiar, is available here.

New to our website this week are five engagement letter templates:

Our Charity Accounting and Charity Audit webinars are available here for immediate access and come with much support material as an extra free bonus and we have several audit template letters for charities that are up to date for SORP, GDPR and Coronavirus (COVID-19), downloadable for immediate tailoring in MS Word.

For a full list of all our webinar recordings, please go to our webinar site here. They may be viewed at any time for 12 months after the date of purchase.

We also have a complete set of charities’ letters of representation in our publications store, updated for SORP and Coronavirus (COVID-19), and letters of engagement for immediate download here. There are also versions available for charities that are not yet implementing the SORP.

by John McCarthy Consulting Ltd. | Sep 13, 2020 | Blog, News

Charities Regulator Report by the Numbers

As we saw in last weeks’ blog there is a wide variety of charity on the Register of Charities in Ireland.

This week we look at the percentage of charities by income and numbers of employees.

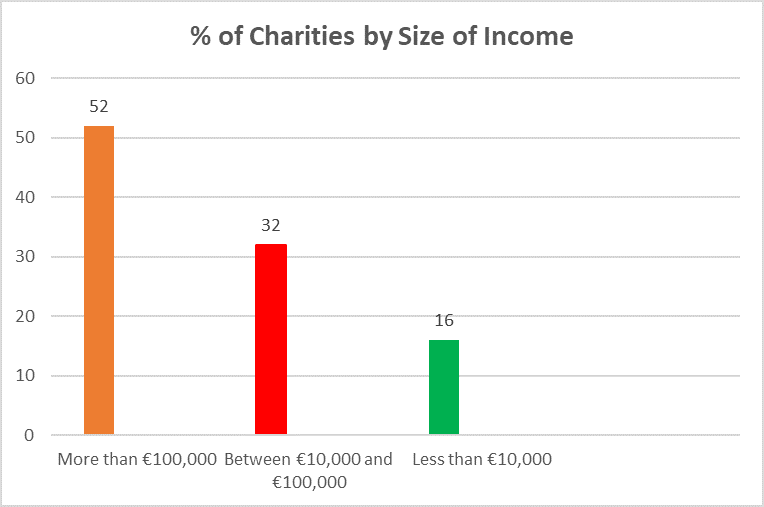

Charities by Income

52% of charities had annual income of more than €100,000, 32% had annual income of between €10,000 and €100,000 while there was a sizeable 16% of charities with income per annum of less than €10,000.

Within the 2,165 charities reporting an annual income of over €250,000 in 2019, 875 (40%) had income in excess of €1 million.

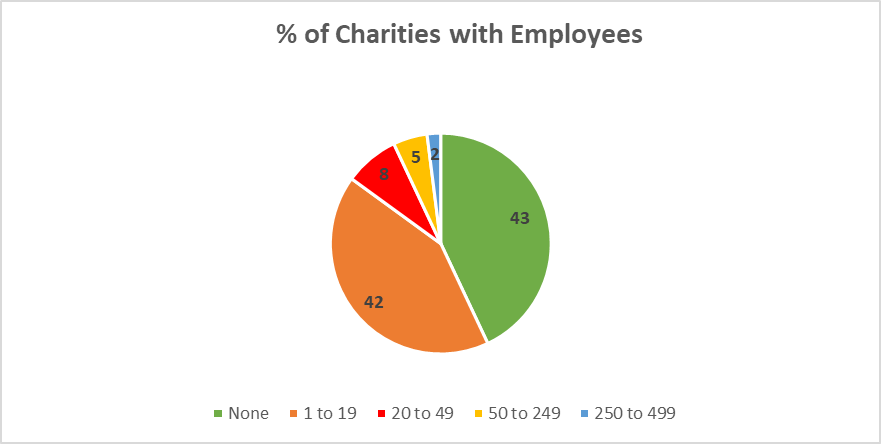

Charities by Employee Numbers

43% of charities had no employees. 42% reported having between 1-19 employees, 8% had between 20-49, 5% had 50-249, while 2% had between 250-499.

The 2019 Charities Regulator Annual Report can be found here.

Our Charity Accounting and Charity Audit webinars are available here for immediate access and come with much support material as an extra free bonus.

We also have several audit template letters for charities that are up to date for FRS 102 SORP, GDPR and Coronavirus (COVID-19) downloadable for immediate tailoring in MS Word.

For a full list of all our webinar recordings, please go to our webinar site here. They may be viewed at any time for 12 months after the date of purchase.

We also have a complete set of charities letters of representation in our publications store, updated for SORP and Coronavirus (COVID-19), and letters of engagement for immediate download here. There are also versions available for charities not yet implementing the SORP.

by John McCarthy Consulting Ltd. | Sep 7, 2020 | Blog, News

Charities Regulator Report

The number of charities registered in Ireland passed the 10,000 mark in 2019 (the actual number was 10,514), according to the Charities Regulator which published its annual report in July 2020.

The Register of Charities

The 10,514 charities on the public Register of Charities at the end of 2019 is an increase of 715 (7%) on 2018. There were 67,129 charity trustees on the Register of Charities at 31 December 2019, up 10% on the previous year. Charity trustees include committee members and company directors who ultimately exercise control and have legal responsibility for running charities.

Points of note from the 2019 Annual Report are:

The most common charitable purposes of registered charities in 2019 were:

- Benefit to the community 54%,

- Advancement of education 30%

- Relief of poverty/economic hardship 9%

- Religion 7%

Breakdown of charities

- Incorporated companies 44%

- Unincorporated entities:

- Associations 15%

- Boards of Management (Schools/other) 27%

- Other 8%

- Charitable Trusts 6%

The full list of the Irish registered Charities can be accessed here on the Register of Charities:

The 2019 Charities Regulator Annual Report can be found here

Our Charity Accounting and Charity Audit webinars are available here for immediate access and come with much support material as an extra free bonus.

We also have several audit template letters for charities that are up to date for SORP, GDPR and Coronavirus (COVID-19) downloadable for immediate tailoring in MS Word.

For a full list of all our webinar recordings, please go to our webinar site here. They may be viewed at any time for 12 months after the date of purchase.

We also have a complete set of charities letters of representation in our publications store, updated for SORP and Coronavirus (COVID-19), and letters of engagement for immediate download here. There are also versions available for charities not yet implementing the SORP.

by John McCarthy Consulting Ltd. | Feb 25, 2020 | Blog, News

Many accountants and auditors are working hard this week to assist primary and post-primary schools around Ireland meet the 28 February 2020 deadline set by the Financial Support Services Unit (FSSU) for the filing of schools’ annual financial statements.

The Education Act, 1998 (the Act) is the relevant legislation that governs this area but it’s out of line with the latest thinking on accounting and legal language used in the Companies Act, 2014 in Ireland.

When compared to this later legislation, The Education Act is found to be inadequate in at least these three areas:

- The Act speaks about ‘all proper and usual accounts’ instead of ‘adequate accounting records’ used in the Companies Act, 2014;

- The Act, is vague about whether the financial statements should give a ‘true and fair view’, which, clearly, they should;

- The Act does not specify precisely the financial reporting framework that ought to be best applied to school accounting, which is now FRS 102, (The Financial Reporting Standard Applicable in the UK and the Republic of Ireland).

This single financial reporting standard applies to the financial statements of entities that are not applying EU-adopted IFRS, FRS 101 or FRS 105. It came into being in 2015, and Section 1A of that Standard came into being in January 2017, well after the Education Act was written. FRS 102 replaced the earlier version of Irish Generally Accepted Accounting Practice (GAAP), to which the Act refers, which had been in place for about 45 years.

New International Audit Standards (ISAs) were enacted for Ireland in June 2016 and the Act does not refer to these either.

Interim solution for Accountants / Auditors

Clearly the Education Act, 1998 needs a refresh from an accounting and audit perspective. In the meantime, these deficiencies are causing a technical difficulty for reporting accountants and auditors in helping schools meet the February deadline.

In an effort to help reporting accountants with this work, we have created a set of four templates, which address the inadequacies of the Act and clarify state how best to achieve a true and fair view in the midst of these inadequacies, through greater disclosure etc.

The templates are:

- Audit assignment engagement letter template under FRS 102

- Audit assignment representation letter template under FRS 102

- Audit exempt compilation assignment engagement letter template under FRS 102

- Audit exempt compilation assignment representation letter template under FRS 102

They templates are available for purchase on our website here for €50 each and may be downloaded immediately as Word templates for easy adaptation.

Have you prepared an AML Business-Wide Risk Assessment which is required if you have an AML Inspection visit? There is a template available and a webinar on how to prepare it. Both of these help firms comply with the latest requirements of Section 30A of the Criminal Justice (Money Laundering and Terrorist Financing) Acts, 2010 to 2018.

For many other webinar topics including Investment Property Accounting, FRS 105, Common Errors in FRS 102 Accounting and the latest on FRS 105 and company law, visit our online webinar training website.

by John McCarthy Consulting Ltd. | Nov 22, 2017 | News

The new Companies (Accounting) Act, 2017 came into effect from 9 June 2017. It has brought with it, some strange consequences for micro-companies, in particular.

The Act brings into law a new accounting standard for measurement and presentation called FRS 105.

This essentially new accounting framework, among other things, will mean that certain qualifying ‘micro’ companies will not have to disclose details of directors’ remuneration, profit and loss account or include a director’s report in their filed financial accounts. Importantly the standard is not available to charities and not for profit entities and regulated entities. It cannot be used by groups and cannot be used if the micro-entity is being consolidated.

Another issue that arises, is that financial statements prepared under FRS 105 are deemed to automatically give a ‘true and fair view’ without the addition of further explanatory notes beyond those set out in company law, under the Companies (Accounting) Act, 2017. FRS 105 is therefore deemed to be a ‘compliance framework’ and not a ‘fair presentation’ framework (as FRS 102 is). Letters of engagement and representation with clients, using FRS 105, will need amended to make this point clear. Amended letters are available by contacting us here.

Let’s explain these two types of accounting framework:

A ‘fair presentation’ framework (e.g. FRS 102) is one that requires compliance with the provisions of the framework but in addition that it acknowledges that in achieving fair presentation, management might have to make additional disclosures that are not specifically required by the framework and, in extremely rare circumstances, it might be necessary to depart from the requirements of the framework to achieve fair presentation of the entity’s financial position and performance in the financial statements.

A ‘compliance framework’, on the other hand, requires compliance with the provisions of the framework i.e. strict adherence to certain rules is required and the preparers of the financial statements have no choice but to follow the requirements of the framework.

To hear more about this and the latest Accounting Update, come to our next CPD course on Monday 27 November 2017 at the Talbot Hotel Stillorgan.

Click here for details and booking on all November courses.